3 Elements of apparel costing process for merchandiser

Introduction

The costing of apparel and textile products is a complex process as it involves a lot of activities associated with each product. In this article will be discusses the elements of apparel costing for merchandisers in the apparel industry. Cost is determined in a variety of ways depending on the nature of the industry, the type of product, the method of production, and the meaning or sense of the term cost. Let’s first understand what is costing before discussing elements of apparel costing.

What is costing???

According to the Chartered Institute of Management Accountants (CIMA), the definition of cost is as follows: “ The technique and process of ascertaining costs”. Another way, “costing is the technique and process of estimating the cost for a product or service or process” defined by Institute of Cost and Management Accountants, London.

There are several elements to apparel costing process, since fashion changes every season and sometimes very frequently, so the product the manufacturer receives for manufacturing from the buyer also changes every season. Let’s see the elements of apparel costing process now. Every merchandiser in the apparel industry must know these elements of apparel costing process.

Elements of Apparel Costing Process

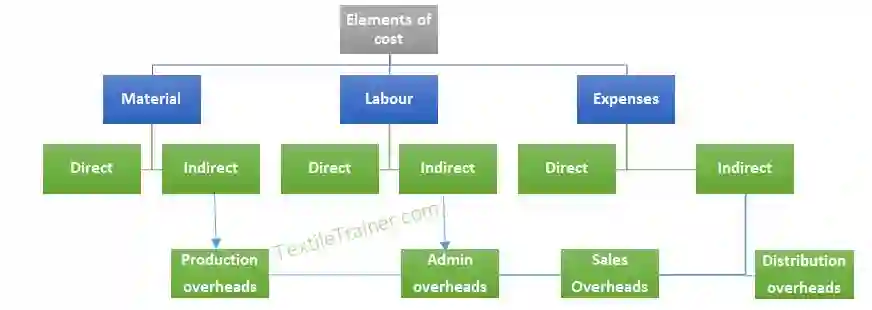

The fundamental elements of apparel costing process are material, labour, and expenses. Following are explains the elements of apparel costing process involved in the basic apparel costing process.

Material Cost

Generally, it refers to the cost of commodities supplied to an undertaking. In addition to procurement and freight inward costs, taxes and insurance, material costs include these activities because they directly contribute to the acquisition of materials. There are two categories of material costs. They are:

- Direct material cost

- Indirect material cost.

1. Direct Material Cost

The direct material cost is the cost of all materials which become an important component of the finished product and the direct material costs are attributed directly and completely to the specific physical units. These materials refer to as direct material costs. Some of the materials that is fall under this category are:

- Materials which specifically purchase, acquired or produced for a particular job, order or process.

- Primary packing materials (e.g. Carton, wrapping, cardboard, etc.)

- Materials passing from one process to another as inputs.

2. Indirect Material Cost

The term “indirect materials” refers to all materials that cannot easily assign to specific physical units. These items will not be a part of the finished product. Indirect material cost include consumables, lubricant oil, stationary equipment, and machinery spare parts.

Labour Cost

The effort placed by workers in converting materials into finished products or performing various jobs in a business is referred to as labour. The cost of labour can be further divided into two categories.

- Direct labour cost

- Indirect labour cost

1. Direct Labour Cost

Workers who are directly involved in converting raw materials into finished products are paid direct labour costs, which include wages, salaries, bonuses, or commissions. Direct wages or direct labour cost are the wages paid to skilled or unskilled workers for manual or mechanical work for operating machinery. They can be allocated to a particular unit of production.

2. Indirect Labour Cost

The worker employed to perform work which is not a part of manufacturing of the end product but only to assist the product or operations is known as indirect labour. Indirect labour costs are those engaged in office work, sales and distribution. For example, a driver of a delivery van paid a salary is a indirect labour cost.

Expenses

“Expenses” are all expenditures other than material and labour incurred in the manufacturing process or rendering of a service. As defined by CIMA, expenses are “the cost of services provided to an undertaking and the notional cost of using owned assets”. Expenses also divided into two categories. They are:

- Direct expenses

- Indirect expenses

1. Direct Expenses

The term “direct expenses” refers to expenses that are specifically incurred and can be directly attributed to a specific product, service or job. A few examples would be the hire charges for special machinery, the carriage inward, royalties, and the costs of special and specific drawings.

2. Indirect Expenses

All expenses excluding indirect material and indirect labour, which cannot be directly and wholly attributed to particular product, job or service, are termed as indirect expenses. For example: repairs to machinery, insurance, lighting and rent of the buildings.

Overheads Cost

Indirect expenses are called overheads cost, which include material and labour.

Overheads= Indirect material+ Indirect labours+ Indirect expenses

Overheads cost can be classified into five:

- Production or manufacturing overheads: connected with factory production function like indirect labour and material cost.

- Administrative expenses: indirect expenditures incurred in general administrative function, they don’t have any direct connection with production or sales activity. Example of administrative expenses are stationeries used, sweeping brooms, salary of a peon.

- Selling expenses: it is the cost of promoting the sales and retaining the customers. For example: advertisement and gifts.

- Distribution expenses: all the expenses incurred from the time of the production completion to the time it reaches its destination. For example: packing material, salary of drivers and insurance of the goods.

- Research and development expenses: any expenses associated with the research and development of a company’s goods or services.

Formula of Apparel Costing Process in Apparel Industry

Formula of apparel costing process in apparel industry is given below.

- Prime cost= Direct expenses + Direct labour cost + Direct material cost

- Overheads= Indirect material cost + Indirect labour cost + Indirect expenses

- Factory cost= Factory overheads cost + Prime cost

- Cost of production= Factory cost + Office and administrative overheads

- Sales cost= Selling and distribution overheads cost + Cost of production

- Cost/ Unit= Selling price ÷ Total Production

Apparel Cost Components

Depending on the style complexity, the number of operations in each process determines the cost. The various apparel cost components include:

- Types of fabric

- Trims type and numbers

- Cutting, making checking and packing charges

- Value added services- printing, embroidery, washing

- Testing of the garment

- Quality parameters expected

- Transportation and logistics cost

- Profit of the manufacturing organisation.

Factors Influencing the Apparel Costing Process

Below are a few other factors that will directly affect an apparel product’s cost.

- Fabric cost: Generally, fabric makes up 60%-70% of the cost of basic styled garments. The types of fabric used in the garment determine the price of the fabric.

- Unit of Measurement (UOM): A merchandiser should also be aware of the cost associated with raw materials. Often, the price is dependent on the quantity of raw material available.

- Fabric Minimum Order Quantity (MOQ): The MOQ is the smallest or minimum quantity that can be purchased from the vendor for any raw material. When ordering fabric, the MOQ plays an important role because it directly affects the price of the garment. When the order of fabric is below the estimated MOQ, the vendor charges a higher amount than regular charges. In estimating small quantity orders, merchandisers need to keep the MOQ in mind.

- Order quantity: A material’s cost is largely determined by its quantity ordered. The higher the order quantity, the cheaper it will be.

- INCO terms (International commercial terms): A major factor in determining the cost of a product is the type of agreement between the buyer and seller regarding its commercial aspects. Examples include FOB and FAS agreements.

Conclusion

These are the elements of apparel costing process which is used in apparel industry. Beside, here discussed factors that are influenced the apparel costing process. If you have any question about these article, feel free to ask me below comment box.

Reference

- Jeremy A. Rosenau, David L. Wilson, (2007), Apparel Merchandising- The line stars here. Fairchild publications, New York.

- R. Rathinamoorthy, R. S. (2018). Apparel Merchandising. Chennai: Woodhead Publishing India Pvt. Ltd.

- Grace I. Kunz, Ruth E. Glock, (2004), Apparel Manufacturing: Sewn Product Analysis. 4th Edition. Prentice Hall.

You May Read

- 3 Easy Supplier Evaluation Methods Used in Apparel Industry

- 4 Most Important Factor for Supplier Evaluation in Apparel Industry

- Apparel Analysis with Example : Easy 7 Steps of Polo Shirt Analysis

- 50 Terminologies Used in Merchandising in Apparel Industry: Most Useful

- Exploring Innovative 4 Alternative Methods of Fabric Joining

- Best 10 Differences Between Sewing Method and Alternative Method of Fabric Joining

- Study on Industrial sewing machines: A Comprehensive Guide to Types and Application in Apparel Manufacturing